The Covid-19 pandemic took the world by surprise with an unprecedented political and economic shock. As a result, we’ve updated our outlook on digital currency attitudes and trajectories

CBDC – as we knew it

Two months ago, the factors that drove research and development into central bank digital currencies (CBDC) included:

- Technology considerations: the possibilities unlocked by today’s tech to create e.g. programmable money and decentralised, even offline exchange infrastructures;

- Efficiency and financial inclusion: the desire to develop payment systems and use them as a development tool for the rest of the economy (less of a driver in developed economies);

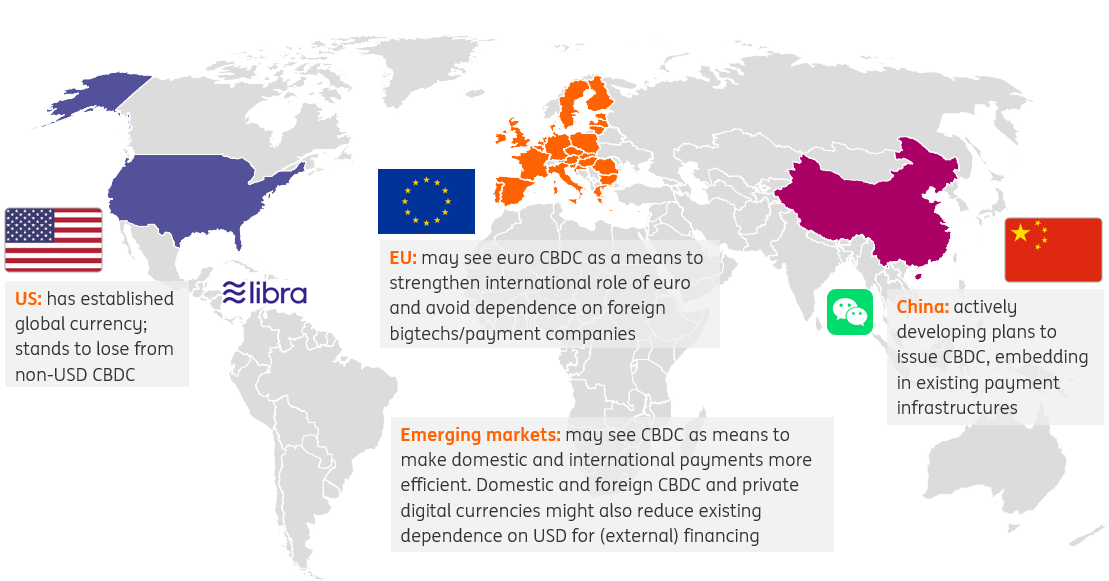

- Geostrategic considerations: the dominance of the dollar in finance and trade, the emergence of China on the world stage and the role of US and Chinese big tech firms;

- Monetary autonomy: the dystopian idea of a private sector global currency operator sharply reducing national central banks’ monetary degrees of freedom and efficacy;

- The declining use of physical cash and the urge to develop public sector alternatives to private digital infrastructures;

- The realisation that any CBDC is potentially highly disruptive and therefore has financial stability implications that need to be managed carefully.

Covid-19 will accelerate, not slow, CBDC developments

We don’t think that Covid-19 alone will be a good enough reason for central banks to suddenly adopt digital currencies. However, the pandemic is likely to accelerate the process.

Here are a few reasons:

- The declining use of physical cash is likely to accelerate, as contactless payments are encouraged to reduce contagion risk. While this may not win over the staunchest physical cash fans, the forced introduction to contactless payments may convince a silent majority;

- The role of government is likely to increase, as we discuss here. This may make it easier for central banks to obtain the necessary political mandate to introduce a digital currency;

The pandemic may clear the political way towards introduction of CBDC

- The financial system will come under increased pressure from Covid-19. The financial stability concerns related to CBDC (mainly substitution from bank deposits into CBDC) will therefore be even more pressing. At the same time, so will be calls to insulate payment systems from pressures in the lending parts of the financial system;

- The pandemic will reshuffle the cards on the geopolitical stage. Some countries may emerge with less economic damage, giving them a clear opportunity to flex their muscles;

- This and de-globalisation may intensify attempts to establish “national champions” in digital payments, either private or public.

So what are central banks up to? Will Libra 2.0 host any CBDC?

The global Financial Stability Board launched a consultation on global stablecoins (such as Libra), however, that was already planned. The Dutch central bank stated this week it’s ready to test CBDC in the Netherlands, once CBDC is properly debated at the Eurozone level. Yet this statement too, like other communications about intensifying research and pilots starting, was already in the pipeline before Covid-19. In other words, it’s too soon to see a corona effect.

De-globalisation may intensify attempts to establish “national champions” in digital payments

Last week the Libra association updated their white paper and introduced “single-currency stablecoins” alongside the original multi-currency Libra coin. In this new version, they argue that if central banks were to create a digital dollar, euro or British Pound, the Libra association could host these on the Libra infrastructure.

This offer has put the ball firmly back in the central bankers’ court. It may sound like an offer central banks can’t refuse, but we doubt whether they will take it up. In principle, a central bank may like the idea of having its CBDC hosted on multiple private platforms, in addition to its own public infrastructure. Availability on widely used platforms is in fact necessary for broad CBDC acceptance. So from that perspective, hosting CBDC on the Libra platform may be fine. There are a few problems though.

The dreaded multi-currency original Libra is not off the table yet. Authorities will continue to regard this global stablecoin with suspicion

The biggest one is that, even though Libra added single-currency Libra’s and potentially CBDC to the mix, the dreaded multi-currency original is not off the table yet. Authorities will continue to look at this global stablecoin with suspicion, and will probably demand guarantees in some form that it does not threaten monetary autonomy. We doubt whether Libra is able and willing to give such guarantees. The best one, from the authorities’ perspective, is to have no multi-currency Libra at all. But even in this long-awaited version 2.0, Libra refused to bite that bullet.

Moreover, Libra 2.0, which still has the potential to quickly become a dominant payment platform, will not make the previously mentioned questions on financial stability any easier. The Libra association may feel it has addressed all authorities’ objections to its v1.0 proposal, yet it may face more stiff conversations with central bankers.

A new dynamic?

In the end, whether CBDC arrives or not, was never, and never will be, a purely technological question. It was and will primarily be about political acceptance and alignment with other political strategic goals, both domestic and international.

De-globalisation, bigger role of governments and close cooperation with the financial sector will guide CBDC discussions

In that respect, our initial assessment is that CBDC will be a more likely option post-Covid-19. The bigger role of governments and the close cooperation between them and the financial sector in combating the economic fallout will guide discussions about CBDC in the context of the role the financial sector has in serving society.

That said, CBDC will not be introduced overnight. Right now, authorities and the rest of society are in crisis-fighting mode. However, previous crisis episodes have shown us that the foundations for the post-crisis institutional framework are laid in crisis times. We expect the debate to start soon.

This article first appeared on ING THINK